You may be eligible for retirement benefits if you are a military member. So, how to calculate military retirement? To calculate your military retirement, you will need to know your years of service and your age at retirement. You will also need to know whether you qualify for a pension or not. If you do not qualify for a pension, you may still be eligible for other benefits.

Computing Retired Military Pay

Understanding and calculating military retirement pay might be difficult. Depending on when you joined the military, you may be eligible for a bonus, to contribute to the Thrift Savings Plan, or to receive a lump-sum payout. Which is the best solution for you? We explain this in this section.

Military Retirement Pay Options

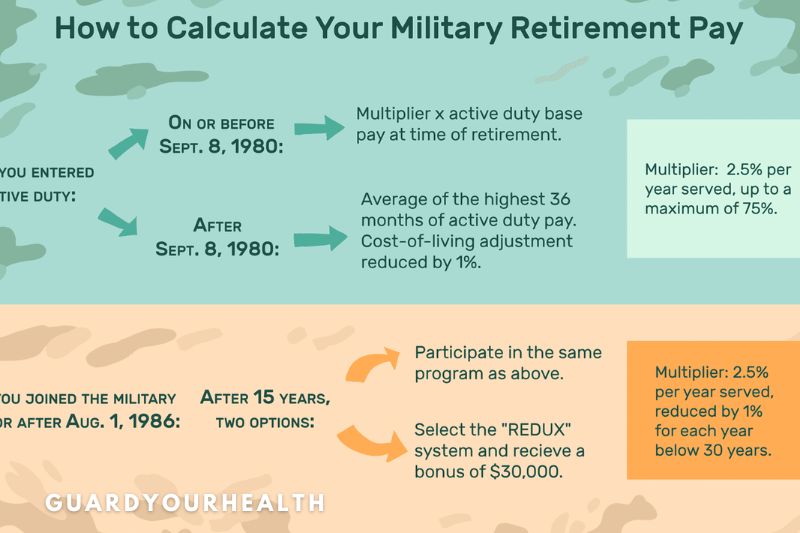

There are four schemes for how to calculate military retirement pay compensation. What you use and whether you have a choice depends on when you joined the military. Those who joined the military before 1986 are eligible for either the Final Pay Retirement System or the High 36 Retirement System. Those who joined after January 1, 2018, are part of the Blended Retirement System.

Those who joined the service between August 1, 1986, and December 31, 2017, may choose between the CSB/REDUX Retirement System and the Blended Retirement System. Which system is the best fit for you? To find out more, keep reading.

Final Pay Retirement System

Service personnel who joined the military before September 8, 1980, and are currently serving may use the Final Pay Calculator to determine their future military pension amount. The High-3 calculator is used by military personnel who enlisted after September 8, 1980.

The Final Pay method employs the simplest formula of any retirement plan. For each year of service, you will get 2.5 percent of your last monthly basic salary. For example, if you retire after 40 years of active service, you may expect to earn a retirement pension equal to 100 percent of your monthly base salary.

You’ll input the identical information for the Final Pay calculation as the other service members did for the High-3 calculator.

By altering the factors, you may also reset the calculator’s findings. Delaying your retirement year, for example, may result in a higher base salary owing to automatic cost-of-living increases, even if you do not get a promotion. This would boost your retirement income.

If you joined after 2018, you should use the Blended Retirement System calculations for active duty, National Guard, or reserves.

Did you know that Military OneSource provides free financial advice via phone, chat, or secure video conference to all active-duty service personnel and their immediate families?

They may go through your High-3 or Final Pay calculator projections and provide recommendations on making the most of your eventual retirement pensions. You may also visit your on-base financial, military officer retirement pay scale for free in-person assistance in determining your retirement plans and payments.

Remember how to calculate navy retirement pay, the more money you’ll have when you get there.

High 36 Retirement System

You are qualified for the High 36 Retirement System if you joined the service between September 8, 1980, and July 31, 1986.

The High 36 retirement system is identical to the Final Pay Retirement System described above, except that retired pay is calculated using the average base pay for your three best paid years (36 months) rather than final monthly base pay.

If you retire after 20 years of service, you will get 50% of your average highest 36 months base salary, or 100% if you resign after 40 years. Your three highest-paid years are often your last three years of active service, although, in many pay grades, you may have hit the maximum compensation many years before retiring.

CSB/REDUX Retirement System

If you joined the service between August 1, 1986, and December 31, 2017, you are eligible for either the CSB/REDUX Retirement Scheme or the High 36 system.

The CSB/REDUX system bases your pension on the average of your top 36 months’ base salary, as described above, but the similarities end there. When you reach your 15th service anniversary, the CSB/REDUX system awards you a “Career Status Bonus” (CSB) but also decreases (REDUX) your retirement income.

Under the CSB/REDUX, you will get a $30K cash incentive (about $21K after taxes), and your retirement percentage will be decreased from the standard 2.5 percent for each year of service by an amount equivalent to 1% for each year of service less than 30 years.

This means that if you retire after 20 years, you will receive 40% of your base pay – (30 years minus 20 years = ten years, the normal High 36 retirement pay at 20 years is 50% of your base pay, BUT under CSB/REDUX, that is reduced by 10% (1 percent for every year of service less than 30), so your retirement pay is only 40% of your base pay.)

This discount does not apply if you have served 30 years or more.

It’s already complex, but it gets worse. The annual cost of living adjustments is made in all retirement schemes. This is a minor yet critical element. The cost of living adjustment may quadruple your retirement check throughout your retirement.

The national Consumer Price Index determines the COLA for the final payment and high 36 systems each year. The COLA for the CSB/REDUX retirement scheme, on the other hand, is the Consumer Price Index minus 1%. So, a retiree under the High 36 plan may enjoy a 1.7 percent COLA increase in their retirement check, but a retiree on the CSB/REDUX plan may only experience a 0.7 percent COLA raise.

There is one additional wrinkle to the COLA for CSB/REDUX retirees. At age 62, the 1% cut is eliminated, resulting in the same monthly salary for High 36 and CSB retirees.

As you can see, it is rather sophisticated; contact your personnel office for more information.

Blended Retirement System (BRS)

You are eligible for the BRS if you join the military for the first time after January 1, 2018. Your pension under the BRS is identical to the CSB/REDUX scheme in that you will get 40% of your basic salary after 20 years. You will also get a bonus after 12 years, typically 2.5 percent of your yearly basic salary, although this number may vary based on the requirements of the service.

The military will contribute 1% of your basic salary to your Thrift Savings Plan (TSP), akin to a savings account or 401(k). You will also immediately register in the TSP, contributing 3% of your basic income. This donation may be increased, decreased, or terminated at any time. After two years of service, the military will match up to 5% of your TSP contribution.

When you retire, you have the option of receiving your entire retirement or a lump-sum payout. If you choose the lump amount, your monthly retirement payment will be lowered until you reach the age of 67. You will also have a large amount of money in your TSP that may be withdrawn tax-free depending on your age.

How to use the High-3 military retirement calculator

If you joined between September 8, 1980, and July 31, 1986, you might use the High-3 Calculator to determine your base salary. After 20 years of service, you will get a pension equivalent to 2.5 percent of your average basic salary for your three highest-paid years, or 36 months, for each year you serve. The plan is frequently referred to as the “High-36.”

For example, if you retire after 20 years of service, your retirement pension will be 50% off your highest 36-month salary average. If you depart after 40 years, your pension will equal 100 percent of your monthly salary average.

You may also receive extra payments if you have opted to contribute to your Thrift Savings Plan.

To see your total predicted retirement payments, utilize the High-3 calculator.

Step one: “Get Started.”

Choose whether you are presently “Active Service” or a “Reserve Component,” then indicate whether you want to retire from active or reserve duty. To demonstrate, we’ll assume retirement from active service.

Then click “Get Started.”

Step two: “Personal Information.”

In this stage, you will enter:

- Your date of birth

- Your pay entrance base date—basically, the month and year you initially received military pay. This is located on your LES.

- Your current salary level

- Your active service date- the month and year you originally went on active duty, which may coincide with your pay entry base date.

- The number of years you intend to service before separating or retiring. It’s OK if you’re unsure; provide your best estimate.

- After you’ve entered your answers, click “Continue.”

Step three: “Retirement Information.”

You may not know the answers to this step right now. Many of these boxes have the most popular pre-filled replies. Begin with the recommended common replies. You may always modify the replies using drop-down options.

You’ll type in your:

- Average life expectancy

- TSP withdrawal age- the age at which you will begin withdrawing funds from your TSP account. This is set at 67, the expected “Full Retirement Age,” however you may begin withdrawing at 5912 years without paying additional income taxes. The more you can wait before withdrawing, the more money you’ll make.

- TSP contribution rate- the proportion of your basic salary that you contribute to your TSP while serving. This is set at 5% by default. However, if you want to deduct more or less money from your monthly salary, you may adjust this amount.

- TSP rate of return- the amount of additional money you expect your retirement account to earn each year before you begin taking from it. This assumes a 7% yearly rise on average. This percentage may be reduced for a more cautious forecast and a smaller future TSP payment. Alternatively, you might raise it if you believe the market will perform better when you withdraw your assets.

- TSP rate of return after withdrawal- the amount you expect your account to earn each year once you start withdrawing. This is set at 3% by default.

- Current TSP account balance- this information is available on the official TSP website.

- After you’ve made your selections, click “Continue.”

Step four: “Career Progression.”

Remember that your final pension rate is determined by your highest 36 months of basic pay. As a result, the calculator asks you what you believe your pay grade will be every year from your estimated separation year.

If you are unsure, the system fills in each year’s prospective pay grade based on a “normal military career progression.” You may continue from here or use the drop-down option to overrule the calculator’s choices.

The High-3 calculator displays your projected retirement benefits in three tabs.

- The first “Overview” page displays how much you may anticipate getting each year from your basic salary, High-3 pension, and TSP withdrawals.

- The “TSP Summary” page displays the entire future value of your TSP account as it rises via investments and decreases through withdrawals.

- The final “All Payments” page displays each year of your predicted service and retirement payments as a table rather than a graph. This includes your pay grades, TSP contributions, and retirement payouts (including pension and TSP).

- You may modify the calculator’s findings by changing your retirement year, potential pay grades, and extra contributions to your TSP account.

For example, you may have first entered your current pay grade. However, assume you’ll receive a promotion with a better starting salary shortly and remain for another three years at that pay grade. This change may enhance your projected retirement income.

If you are in the Guard or reserve, your retirement is calculated differently than if you are active. If you joined before 2018, you might use the REDUX Calculator to determine your non-regular retirement.

How much does a retired e6 make after 20 years?

After 20 years in the Army, your pay is $3,310 per month, or $39,726 per year as a basic, three-stripe sergeant. If you’ve moved up to an E-6 staff sergeant, it’s $3,944 per month, or $47,328 per year.

When Can You Expect Your Retired Military Pay?

Military retirees get paid on the first business day of each month. Payday will be the preceding business day if the first of the month occurs on a weekend or holiday. A list of retired military paydays will assist you in budgeting.

FAQs

1. How much does a retired e6, e7, e8 make after 20 years?

For e6- After 20 years in the Army, your pay is $3,310 per month, or $39,726 per year as a basic, three-stripe sergeant. If you’ve moved up to an E-6 staff sergeant, it’s $3,944 per month, or $47,328 per year.

For e7- $27,827 per year

What is the retirement pay for an E7 with 20 years? As of 2022 the pay calculation projection an E7 retiring with exactly 20 years of service would receive $27,827 per year. It’s important to note the present value of almost $800,000 for a 40 year old receiving this pension indefinitely.

For e8-Final Pay Plan: For Soldiers who entered military service prior to September 8, 1980 retired pay is computed using 50 percent of basic pay after 20 years of service plus an additional 2.5 percent for each additional year.

2. How much does a cw4 make in the army

A Chief Warrant Officer 4 is a warrant officer in the United States Army at DoD paygrade W-4. A Chief Warrant Officer 4 receives a monthly basic pay salary starting at $4,792 per month, with raises up to $8,926 per month once they have served for over 30 years.

3. How much money does a retired Navy make?

The typical US Navy Retired salary is $91,370 per year. Retired salaries at US Navy can range from $50,000 – $288,428 per year.

Conclusion

There are a few different ways how military retirement pay is calculated, but the best way is to use the “High-3” method. This method takes your highest three years of base pay and averages them together to determine your pension amount. Thanks for reading!